Contact

Home Knowledge Base

Sensitivity Analysis in IND AS 19

The Ministry of Corporate Affairs of the Government of India had introduced the Indian Accounting Standards IND AS 19 to prescribe accounting and disclosure norms for employee benefit schemes applicable to business entities registered in India. Under the new IND AS 19 accounting standards, several new requirements are to be disclosed in the actuarial valuation reports. One such requirement is the sensitivity analysis report, under which it is required to show how the defined benefit obligation would have been affected if the actuarial assumptions would undergo a change.

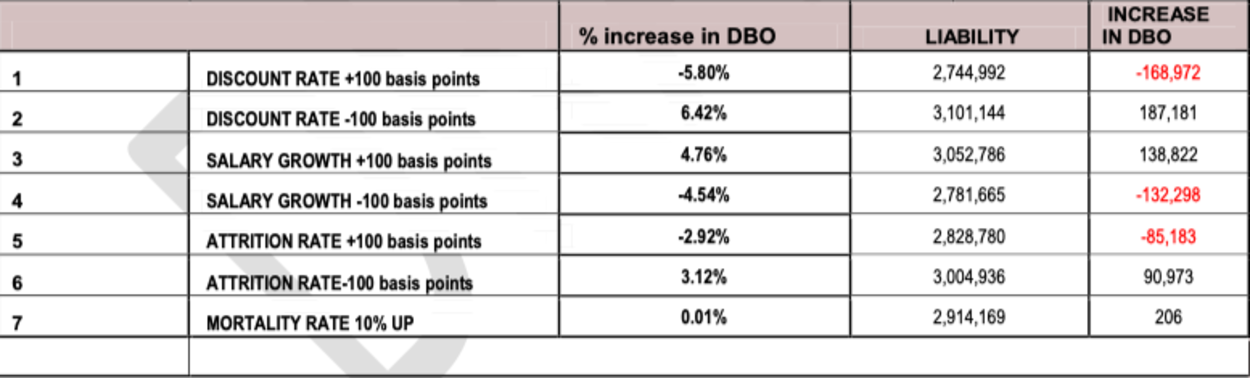

Change in Actuarial AssumptionsA sensitivity analysis report measures how the defined benefit obligation of a reporting entity would change, if the relevant actuarial assumptions undergo change within a specified range (i.e a +/- limit). Paragraph 145 of IND AS 19 mandates that each entity reporting under the IND AS 19 accounting standard shall disclose, at the end of the reporting period, the sensitivity analysis for significant actuarial assumptions that are used in arriving at the valuation - the discounting rate, salary growth rate, attrition rate and mortality rate.

As standard disclosure part of the sensitivity analysis under IND AS 19, we provide the changes in DBO liabilities if the discount rate changes by +/- 100 basis points, salary growth rate increases by +/- 100 basis points, attrition rate increases by +/- 100 basis points and a 10% increase in mortality rate.

Figure: Sensitivity analysis disclosures as per IndAS 19

Figure: Sensitivity analysis disclosures as per IndAS 19

For example, lets say the discount rate at the end of the reporting period was 6.52%, under sensitivity analysis disclosures, it would be required to disclose the liability and increase in DBO/percentage increase in DBO assuming the discount rate is 5.52% (-100 basis points) and 7.52%(+100 basis points) – while assuming all other actuarial assumptions remain the same. Similarly, for attrition rate, salary growth rate etc.

It is to be noted that when performing sensitivity analysis, while one assumption is being tested, all the other assumptions remain the same. However in practice, it is unlikely that changes in assumptions will occur independently. Usually significant change in one assumption due to socio-economic factors also results in changes in other assumptions. However, for the purposes of IND AS 19 reporting, it suffices to test each assumption independently.

+91 936 320 0885

+91 998 027 7885

mail@consultactuary.com

© Copyright 2020. All Rights Reserved Home | Contact Us | Knowledge Base | Privacy | Terms of Use