Contact

Home Knowledge Base

Why is Actuarial Valuation Required?

Actuarial valuation is an accounting exercise performed to estimate future liabilities arising out of benefits that are payable to employees of a company. As per statutory requirements, various forms of benefits are available to the employees of a company. Salaries and leaves are well known forms of employee benefits that are paid to employees of a company for the services rendered by the employees to the company. Examples of other benefits available to employees include gratuity, pensions and provident funds. Some of these benefits like gratuity and pensions are not paid immediately, but accrue over the term of employment of the employee. Hence, they the obligations arising out of these employee benefits need to be estimated and a provision must be made in the book of accounts of the company every year. This exercise is known as actuarial valuation, and is required for regulatory compliance during financial audit of a company.

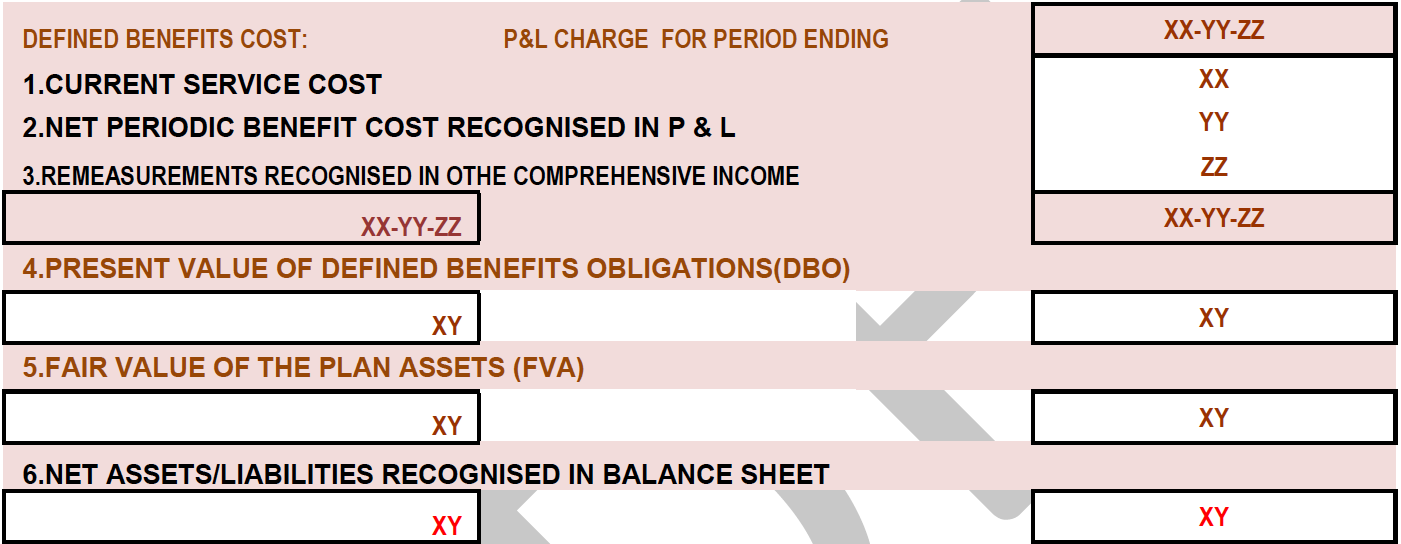

Liability to a company arises when an employee has provided his or her service to a company over a period of time. In the actuarial valuation exercise, a liability payout at a future date is estimated using various assumptions such as discounting rate and salary growth rate. These are termed as “employee benefits”. Actuarial valuation is done to calculate the present-day value of payments that will be made to the employees as part of any employee benefits scheme. These are estimated in accordance with the disclosure requirements of various accounting standards for financial reporting. Figure: Employee Benefit Liabiilties disclosure as part of Actuarial Valuation report

Figure: Employee Benefit Liabiilties disclosure as part of Actuarial Valuation report

One of the goals of actuarial valuation of employee benefits is to ensure that the company considers the benefits payable to employees, so that a situation does not arise where an employee is resigning or retiring but the company does not have the funds to pay the employee’s accrued benefits.

Actuarial valuations are mandated by various accounting standards such as IND AS 19, AS – 15(R) , US-GAAP, IFRS etc. Under these accounting standards, actuarial valuation is performed to estimate the liability and make provisions for the same in the balance sheet. An Actuary performs the actuarial valuation of the various benefits like gratuity, leave, provident fund and provides the estimated liability and associated disclosures that needs to be reported in the financial statements of the company.

Related Topics:

Check the applicability of IND AS 19 to your enterprise

+91 936 320 0885

+91 998 027 7885

mail@consultactuary.com

© Copyright 2020. All Rights Reserved Home | Contact Us | Knowledge Base | Privacy | Terms of Use